Understanding State Finances and the Budgeting Process

Four Main Types of Budgets/Budgeting Methods

There are four common types of budgets that companies use: (1) incremental, (2) activity-based, (3) value proposition, and (4) zero-based. These four budgeting methods each have their own advantages and disadvantages, which will be discussed in more detail in this guide.

Source: CFI's Budgeting & Forecasting Course.

1. Incremental budgeting

Incremental budgeting takes last year's actual figures and adds or subtracts a percentage to obtain the current year's budget. It is the most common method of budgeting because it is simple and easy to understand. Incremental budgeting is appropriate to use if the primarycost drivers Cost Driver A cost driver is the direct cause of a cost, and its effect is on the total cost incurred. For example, if you are to determine the amount of electricity consumed in a particular period, the number of units consumed determines the total bill for electricity. In such a scenario, the units of electricity consumed do not change from year to year. However, there are some problems with using the method:

- It is likely to perpetuate inefficiencies. For example, if a manager knows that there is an opportunity to grow his budget by 10% every year, he will simply take that opportunity to attain a bigger budget, while not putting effort into seeking ways to cut costs or economize.

- It is likely to result in budgetary slack. For example, a manager might overstate the size of the budget that the team actually needs so it appears that the team is always under budget.

- It is also likely to ignore external drivers of activity and performance. For example, there is very high inflation in certain input costs. Incremental budgeting ignores any external factors and simply assumes the cost will grow by, for example, 10% this year.

2. Activity-based budgeting

Activity-based budgeting is a top-down budgeting Top-Down Budgeting Top-down budgeting refers to a budgeting method where senior management prepares a high-level budget for the company. The company's senior management prepares the budget based on its objectives and then passes it on to department managers for implementation. approach that determines the amount of inputs required to support the targets or outputs set by the company. For example, a company sets an output target of $100 million in revenues. The company will need to first determine the activities that need to be undertaken to meet the sales target, and then find out the costs of carrying out these activities.

Source: CFI's Budgeting & Forecasting Course.

3. Value proposition budgeting

In value proposition budgeting, the budgeter considers the following questions:

- Why is this amount included in the budget?

- Does the item create value for customers, staff, or other stakeholders?

- Does the value of the item outweigh its cost? If not, then is there another reason why the cost is justified?

Value proposition budgeting is really a mindset about making sure that everything that is included in the budget delivers value for the business. Value proposition budgeting aims to avoid unnecessary expenditures – although it is not as precisely aimed at that goal as our final budgeting option, zero-based budgeting.

4. Zero-based budgeting

As one of the most commonly used budgeting methods,zero-based budgeting Zero-Based Budgeting Zero-based budgeting (ZBB) is a budgeting technique that allocates funding based on efficiency and necessity rather than on budget history starts with the assumption that all department budgets are zero and must be rebuilt from scratch. Managers must be able to justify every single expense. No expenditures are automatically "okayed". Zero-based budgeting is very tight, aiming to avoid any and all expenditures that are not considered absolutely essential to the company's successful (profitable) operation. This kind of bottom-up budgeting can be a highly effective way to "shake things up".

The zero-based approach is good to use when there is an urgent need for cost containment, for example, in a situation where a company is going through a financial restructuring or a major economic or market downturn that requires it to reduce the budget dramatically.

Zero-based budgeting is best suited for addressing discretionary costs rather than essential operating costs. However, it can be an extremely time-consuming approach, so many companies only use this approach occasionally.

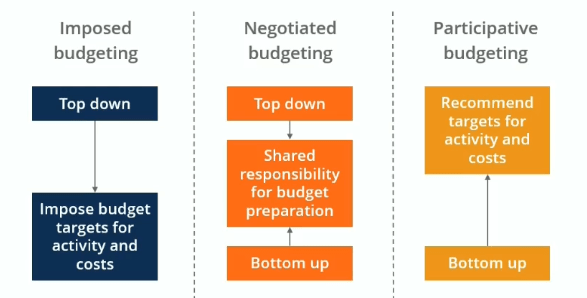

Levels of Involvement in Budgeting Process

We want buy-in and acceptance from the entire organization in the budgeting process, but we also want a well-defined budget and one that is not manipulated by people. There is always a trade-off between goal congruence and involvement. The three themes outlined below need to be taken into consideration with all types of budgets.

Imposed budgeting

Imposed budgeting is a top-down process where executives adhere to a goal that they set for the company. Managers follow the goals and impose budget targets for activities and costs. It can be effective if a company is in a turnaround situation where they need to meet some difficult goals, but there might be very little goal congruence.

Negotiated budgeting

Negotiated budgeting is a combination of both top-down and bottom-up budgeting methods. Executives may outline some of the targets they would like to hit, but at the same time, there is shared responsibility for budget preparation between managers and employees. This increased involvement in the budgeting process by lower-level employees may make it easier to adhere to budget targets, as the employees feel like they have a more personal interest in the success of the budget plan.

Participative budgeting

Participative budgeting is a roll-up approach where employees work from the bottom up to recommend targets to the executives. The executives may provide some input, but they more or less take the recommendations as given by department managers and other employees (within reason, of course). Operations are treated as autonomous subsidiaries and are given a lot of freedom to set up the budget.

Related Reading

Thank you for reading this guide on the four main types of budgeting methods. CFI offers the Financial Modeling & Valuation Analyst (FMVA)® Become a Certified Financial Modeling & Valuation Analyst (FMVA)® CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their financial careers to the next level. To keep learning and advancing your financial education, the following resources are helpful:

- Budget Head Budget Head The person who is ultimately responsible for the framing and creation of the Budget for a project is known as the Budget Head for that project. The Budget itself is a document that lists the expected revenues and expenditures associated with a project.

- Cash Flow Statement Cash Flow Statement A cash flow Statement contains information on how much cash a company generated and used during a given period.

- Operating Budget Operating Budget An operating budget consists of revenues and expenses over a period of time, typically a quarter or a year, which a company uses to plan its operations. Download the Free Excel Template. The monthly budgeting template has a column for each month and totals to be the full year annual figures

- Projecting Balance Sheet Items Projecting Balance Sheet Line Items Projecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

Understanding State Finances and the Budgeting Process

Source: https://corporatefinanceinstitute.com/resources/knowledge/accounting/types-of-budgets-budgeting-methods/

0 Response to "Understanding State Finances and the Budgeting Process"

Post a Comment